To talk about an introduction to econometrics, it is necessary to establish the mathematical and statistical foundations to understand it. Starting from the summation:

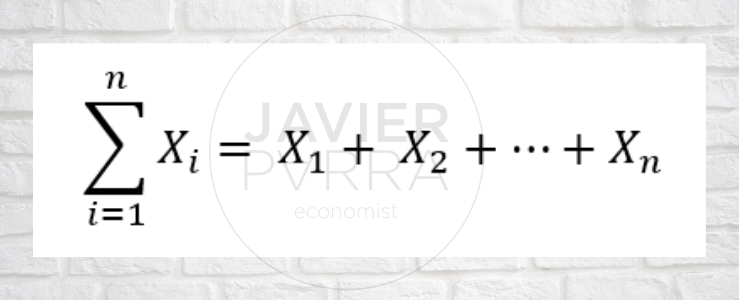

- The symbol Σ is the Greek capital letter sigma and means “the sum of”.

- The letter i is called the summation index; this letter is arbitrary and can also appear as t, j or k.

- The expression ∑(i=1)^n is read as the sum of Xn‘s terms from i equal to one up to n.

- The numbers i and n are the lower bound and upper bound of the summation.

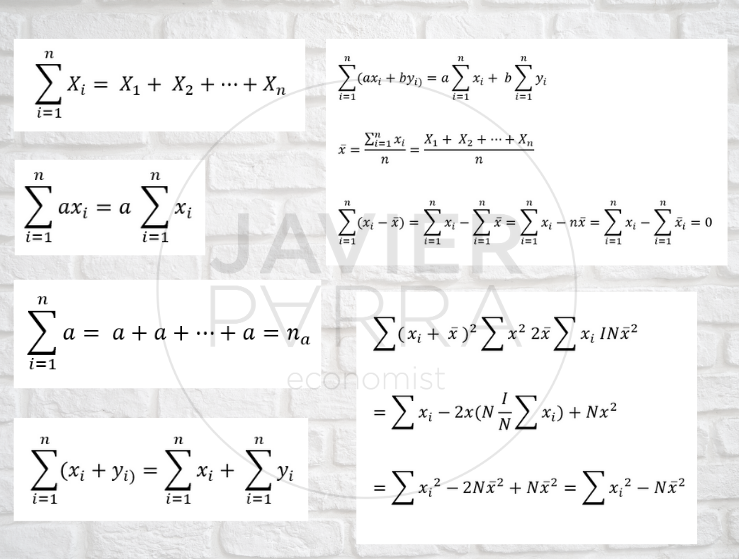

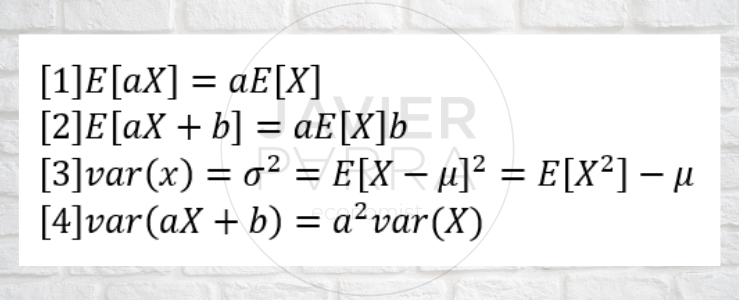

Rules of the addition operation

- A random variable is a variable whose value is unknown until it is observed.

- A discrete random variable can only take a limited or countable number of values.

- A continuous random variable can take any value in an interval.

- The population is the set of individuals who have certain characteristics and are of interest to a researcher.

- The sample is a subset of the population.

Population and sample moments

The sample mean, mean or expected values:

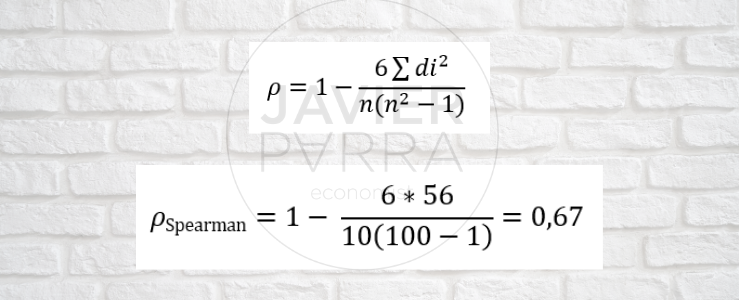

A monotonic relationship is one of the following:

- When the value of one variable increases, so does the value of the other.

- When the value of one variable decreases, the value of the other variable decreases.

Let’s look at the following examples of monotonic and non-monotonic relationships:

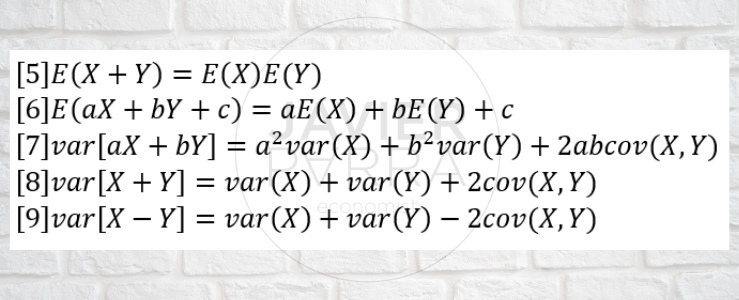

Expected values of the functions of a random variable

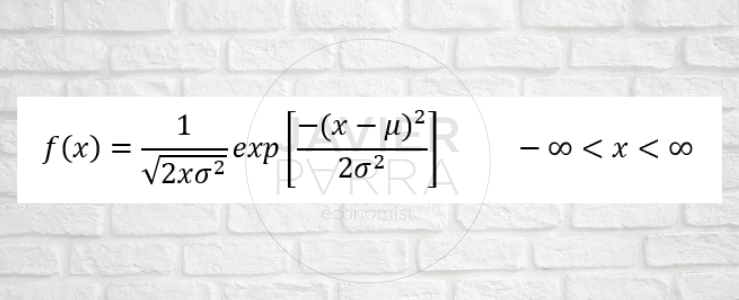

Some important probability distributions

Normal or Gaussian; if X is a normally distributed random variable with mean 𝝻 and variance σ2, it can be symbolised as X~N(𝝻,σ2)

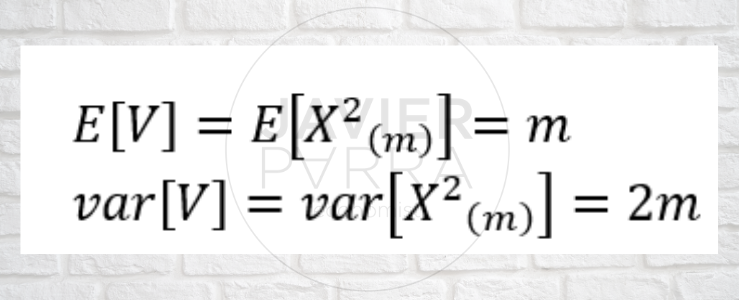

Chi-square: If X, is a normally distributed random variable with mean 0 and variance σ2, then V= X12 +X22 +…+Xm2 ~ X(m)2

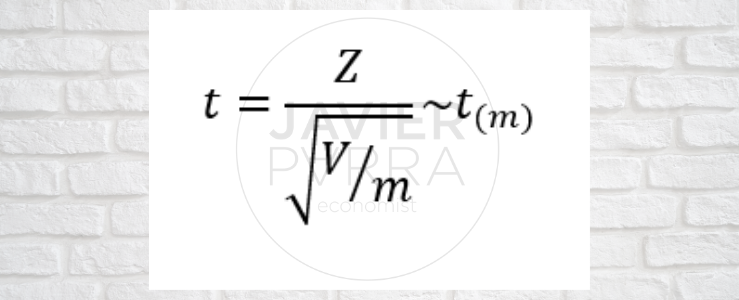

A Student’s random variable is formed by dividing a standard normal random variable with mean 0 and variance 1 by the square root of an independent chi-squared random variable, V, divided by its m degrees of freedom.